How To Do An Adjusted Trial Balance – When you’re ready to adjust your trial balance, you’re ready to prepare your financial statements. The preparation of financial statements is the seventh step in the accounting process. Remember that we need to prepare four financial statements: the income statement, the retained earnings statement, the balance sheet, and the cash flow statement. These financial statements are included in the introduction to the financial statements and in the financial statements for an in-depth discussion of this information.

When preparing the financial statements, the company will review the adjusted trial balance of the account information. From this information, the company will begin to compile all information, starting with the income statement. The income statement will show all the income and expense accounts. The retained earnings statement will include the original retained earnings, total income (losses) (in the loss statement), and dividends. The balance sheet includes assets, intangible assets, liabilities and balance sheets, including expiring liens and common stock.

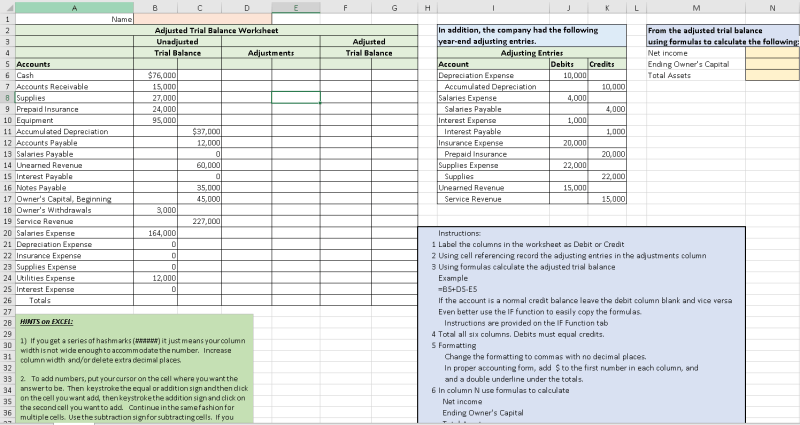

How To Do An Adjusted Trial Balance

Continue to set standards for testing advanced landscape services. The identification of each account’s income statement will continue: balance sheet, income statement, or income statement.

Solved Jung Company Adjusted Trial Balance December 31, 2018

Balance Sheet: Cash, Accounts Receivable, Stationery, Prepayment Insurance, Equipment, Depreciation (Equipment), Inventory, Wages Payable, Unearned Lawn Mowing Revenue Not Found, and General Inventory. Withholding Statement: Distribution. Revenue Details: Lawn Taxes, Gas Taxes, Advertising Taxes, Depreciation (Equipment) Taxes, Inventory Taxes, and Payroll Taxes.

An income statement shows the financial performance of an organization over a period of time. Income will always come before expenses in the presentation of the income statement. Printing Plus is coming in 2019. month of January. input information.

Total revenue was $10,240 and expenses were $5,575. All expenses are subtracted from all income, resulting in an income of $4,665. net income. This amount of income is used to prepare the income statement.

What Is Trial Balance (with Format And Pdf)

Financial statements provide insight into a company’s performance, and investors, lenders, owners, and others rely on the accuracy of this information to make investment, lending, and growth decisions. When one of these statements is incorrect, the financial impact is huge.

For example, Celadon Group reports revenue over a three-year period and revenue growth over those years. The total gross income is about 200-250 million dollars. This gross misrepresentation led to investors being misled and Celadon Group delisted from the New York Stock Exchange. Not only did this negatively impact Celadon Group’s share price and lead to a criminal investigation, but investors and creditors were left wondering what might happen to their investments.

That’s why it’s important to follow the accounting process in detail to reduce errors early on and hopefully avoid misunderstandings that don’t end up in the financial statements. A company must have strong internal controls and best practices to ensure fair disclosure.

Adjusted Trial Balance Printable Pdf Instant Download

A statement of retained earnings (which is often part of a statement of stockholders’ equity) shows how a company’s equity (or value) has changed over time. A second statement of retained earnings is prepared to determine the retained earnings balance for the period. The statement of retained earnings is prepared before the balance sheet because the balance sheet requirement is the final amount of retained earnings. Following is the Post Plus Permanent Earning Details.

Net income figures are taken from the income statement and dividends from the adjusted trial balance as follows.

A record keeping statement always leads to the beginning of accounting. Accounting starts from the end point of the previous period. Since this is the first month in business with Print Plus, there is no opening balance. Calculate the $4,665 of net income from the income statement to the retained earnings statement. Dividends are subtracted from total beginning retained earnings and income to arrive at a January ending balance of $4,565. This retained earnings balance is eventually transferred to the balance sheet.

Prepare Financial Statements Using The Adjusted Trial Balance

The Standards Statements provide guidance to the Financial Accounting Standards Board (FASB) on how to develop accounting standards and consider the scope of financial reporting. To learn more, see FASB’s “Interim Information” page.

The balance sheet is the third statement prepared after the balance sheet and lists the company’s assets (

) on a specific day. Remember, a balance sheet is a balance sheet where assets equal liabilities with stockholders’ equity. The following is the standard for Print Plus.

Solved Presented Below Is The Adjusted Trial Balance Of

The final income statement is taken from the statement of retained earnings and the statement of assets, liabilities and common stock is taken from the adjusted trial balance as follows.

Looking at the asset section of the balance sheet, inventory depreciation is entered as a discordant asset account. Accumulated value ($75) is subtracted from the original cost of the equipment ($3,500) to show the book value of the equipment ($3,425). The balance sheet is adjusted as shown on the balance sheet because total assets are $29,965, as are all liabilities to stockholders.

There is a documentation process that a company will use to ensure that period-end adjustments translate into correct financial statements.

Why Is My Adjusted Trial Balance Not Balanced?

Both U.S. companies and companies headquartered in other countries prepare the same primary financial statements—the income statement, balance sheet, and cash flow statement. The presentation of these three primary financial statements is similar to what should be presented under US GAAP and IFRS, but interesting differences may arise, particularly in the presentation of the balance sheet.

While US GAAP and IFRS require minimum items to be presented in financial statements, such as revenues, expenses, taxes and income, for example, US publicly traded companies have additional requirements with the SEC for financial reporting. For example, IFRS-based financial statements require only current period information and prior period information. US GAAP does not require prior periods to be presented, but the SEC requires companies to present one prior period in the balance sheet and three prior periods in the financial statements. Under IFRS and US GAAP, companies may provide more than the required minimum requirements.

The most significant differences in presentation between the two versions of GAAP are in the balance sheet. There are no specific requirements under US GAAP for how accounts must be presented. However, the SEC requires companies to report balance sheet information in the highest order, which means that assets with cash are listed first because it is the company’s most liquid account. Liquidity refers to how easily an item can be converted into cash. IFRS requires accounts to be classified into current and non-current categories of assets and liabilities, but does not require a specific presentation format. So for American companies, the first item that always appears on the balance sheet is current assets, and the first account balance is cash. This is not always the case under IFRS. Although most international company balance sheets will be presented in the same way as US companies, the lack of required structure means that the company can present both long-term and current assets. A balance sheet under IFRS can be displayed as shown here.

Adjusting Entries And The Accounting Cycle

Study the annual report of Stora Enso, a global company that uses a standardized format for presenting the balance sheet, also known as the statement of financial position. The calculator can be found on page 31 of the report.

Some of the main differences between financial statements prepared under US GAAP and IFRS are primarily related to measurement or timing issues: in other words, how a transaction is measured and when it is recorded.

The 10-column worksheet is an all-in-one spreadsheet that shows the transition of account information from the trial balance to the financial statements. Accountants use a 10-page worksheet to help calculate period-end adjustments. Using the 10-page worksheet is an optional step that companies can use in their accounting process.

Solved] The Following Is The Frederick Company’s Adjusted Trial Balance….

There are five columns, each containing debits and credits, for a total of 10 columns. The five columns are trial balance, adjustment, adjusting trial balance, income statement, and balance sheet. As the company posts its daily journal entries, it can begin to transfer this information to the trial balance column of the 10-page worksheet.

A description of the Printing Plus test parameters was shown earlier. Note that the debit and credit columns are $34,000. If we go back and look at the Printing Plus trial balance, we see that the trial balance shows a debit and credit of exactly $34,000.

Once the trial balance information is on the worksheet, the next step is to populate the balance information from the corrected journal entries.

Solved Adjusted Trial Balance Credit Unadjusted Trial

To get the numbers in these columns, take

Adjusted trial balance worksheet, sample adjusted trial balance, adjusted trial balance to income statement, how to do adjusted trial balance, how to make an adjusted trial balance, adjusted trial balance template, adjusted trial balance template excel, adjusted trial balance closing entries, how to prepare an adjusted trial balance, an adjusted trial balance, unadjusted trial balance to adjusted trial balance, the adjusted trial balance